What is Stablecoin Settlement?

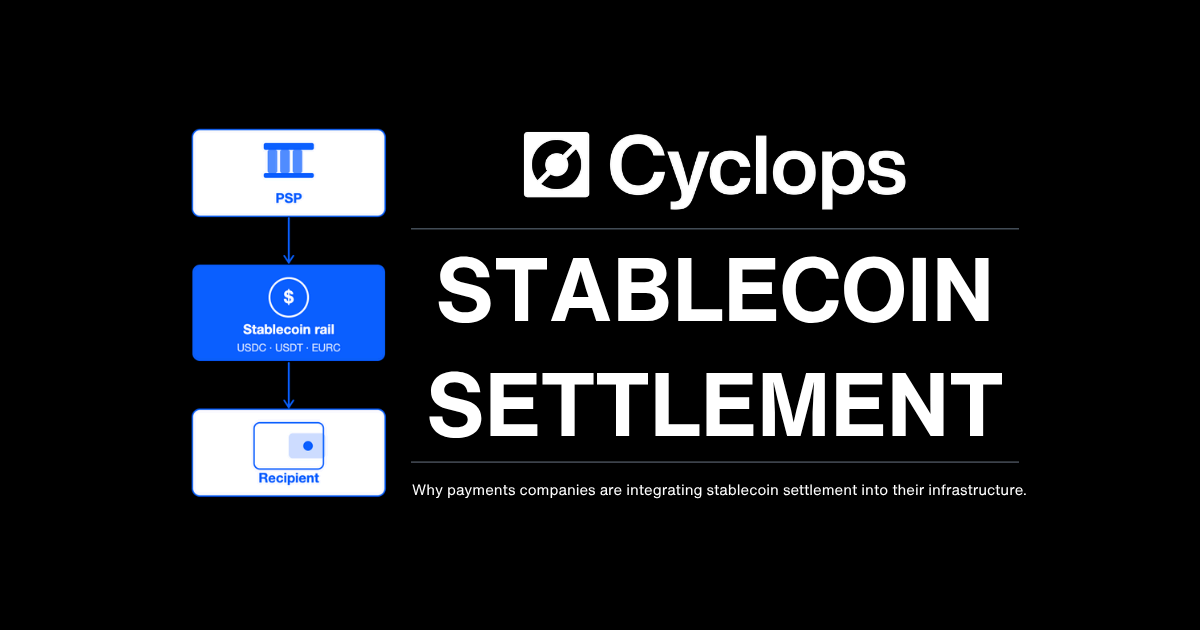

Why payments companies are integrating stablecoin settlement into their infrastructure.

In payments, settlement is where some of the worst operational pain can live. Complex stacks, FX conversion at every turn, cut-off windows that stop the clock on Friday afternoon and pre-funded accounts tying up working capital across multiple jurisdictions. Every PSP doing any cross-border settlement at scale knows this friction. It's expensive, slow and structurally resistant to improvement within the legacy model.

Stablecoin settlement emerged because the existing system has real, measurable problems — and the industry finally has the infrastructure to do something about them.

What Is Stablecoin Settlement?

When a transaction settles, funds move from one party to another through a defined set of rails. Traditional settlement runs through banking infrastructure — correspondent banks, intermediaries, cut-off schedules and multi-day clearing windows. It works, but it is slow, expensive and built for a world where moving money internationally was genuinely difficult.

Stablecoin settlement supplements those rails with blockchain-based transfers of fiat-backed tokens. Here is how it works in practice: a PSP receives payment from a consumer or business, converts the proceeds into a stablecoin like USDC, USDT or EURC and transfers those tokens on-chain to the merchant. The merchant can hold the stablecoin, convert it back to local fiat currency or use it for the next transaction in the flow. The entire process is transparent, verifiable and settled in minutes rather than days.

- No need for correspondent banks to approve transfers.

- No compounding intermediaries taking cuts along the way.

- No clearing windows restricting when the funds actually arrive.

The blockchains are the ledger, the stablecoins are the currency and the settlement is final when the transaction confirms on-chain — typically within seconds to a few minutes.

The outcome is the same as traditional settlement: funds move from one party to another, but the mechanics are fundamentally different.

Why Payments Companies Are Using It

24/7 Settlement

Legacy rails have a schedule. They stop on Friday afternoon and don't restart until Monday morning. Public holidays create multi-day gaps. For merchants operating globally across time zones, that means capital sitting idle, reconciliation headaches and cash flow unpredictability that is difficult to manage at scale.

Stablecoin settlement runs continuously with no cut-off windows, weekend delays or holiday schedules. Funds settle when the transaction happens.

Cross-Border Without the Friction

Cross-border settlement through traditional rails means correspondent banking relationships, FX conversion at multiple points and fees that stack up fast. According to the World Bank's Remittance Prices Worldwide report, the global average cost of sending a cross-border payment sits at 6.36%, with banks averaging 14.55% per transaction. On stablecoin rails, the all-in cost in most corridors runs under 1%. For a PSP moving serious cross-border volume, that difference compounds quickly.

Beyond cost, stablecoin rails open corridors that traditional banking infrastructure can't serve efficiently. Markets where correspondent banking is unreliable, expensive or unavailable entirely become accessible without the overhead of establishing local banking relationships in every jurisdiction.

Breaking the Fiat Trap

Pre-funded accounts represent one of the most expensive problems in cross-border payments. PSPs operating across multiple markets often need separate banking relationships in each one, with capital locked in local accounts to cover settlement obligations. That working capital isn't earning anything, isn't flexible and managing it across a growing number of corridors adds operational complexity.

Stablecoin settlement collapses this complexity. Hold balances in a single denomination, convert at the right moment and settle across corridors from a single platform — without maintaining local banking infrastructure in every market you serve.

How Cyclops Built the Best-In-Class Solution for These Problems

Cyclops identified the core infrastructure needs, as well as the myriad operational concerns, and built the first payments company specific solution that closes all the gaps.

Our platform wasn't built from the outside looking in. Before founding Cyclops, the team spent four years leading the crypto and stablecoin infrastructure team at Shift4. Before that, five years building a crypto payments platform of their own from scratch. They lived through every one of the problems described above, working with the existing infrastructure to try to solve them.

What became clear through that experience was that the available solutions weren't built for payments companies. They were built for banks, exchanges or direct-to-merchant use cases — and payments companies were left trying to make generalist platforms fit their specific requirements. The reconciliation workflows were wrong, the APIs weren't designed for PSP use cases and the support didn't understand the industry.

Cyclops was built to fix that. Every product decision — from how settlement is initiated, to how reconciliation works, to how compliance is handled across jurisdictions — was designed around the specific operational requirements of payments companies. Not adapted from something else, but built from scratch for this problem.

The result is stablecoin settlement infrastructure that payments companies can easily operate without becoming a crypto company in the process.

Want to learn more about the Cyclops platform? Connect with us here.